For a few months now, I’ve been referring to today’s heightened geopolitical climate as the “new red Cold War,” where artificial intelligence (AI)—not necessarily fighter jets and nuclear weapons—serves as the primary battleground between the U.S. and its adversaries, most notably Russia and China.

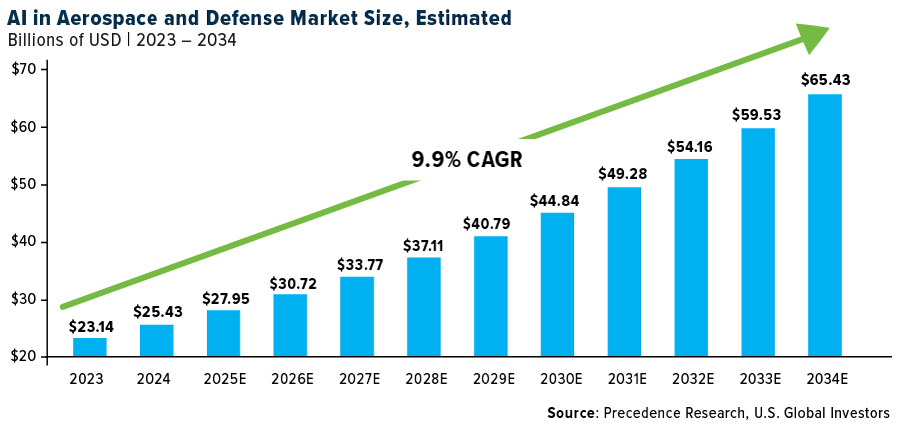

The numbers tell a compelling story. According to one research firm, the global AI market in aerospace and defense is projected to surge from approximately $28 billion today to a staggering $65 billion by 2034. That's a solid 9.91% compound annual growth rate (CAGR). North America alone represents $10.43 billion of this market, and it's growing even faster at 10.02% annually.

Palantir’s Meteoric Rise

We're seeing a dramatic reshuffling of the traditional defense sector hierarchy.

Take Palantir Technologies (NASDAQ:PLTR). The AI-focused company—founded in 2003 by Peter Thiel, among others, and named for a magical artifact from Lord of the Rings—has seen its stock soar approximately 61% so far this year, after returning a massive 340% in 2024.

Meanwhile, traditional defense giants like Lockheed Martin (NYSE:LMT), Northrop Grumman (NYSE:NOC) and General Dynamics have been struggling, with their combined market value now lower than that of Palantir, whose chief technology officer, Shyam Sankar, recently called the competition between the U.S. and China an “AI arms race.”

And let’s not discount the influence of Elon Musk's cost-cutting Department of Government Efficiency (DOGE) initiative. We could see a push to modernize military procurement, prioritizing software, drones and robots over traditional hardware. DOGE has already sent tremors through the defense sector, with traditional contractor stocks taking hits as new players like SpaceX, OpenAI and Anduril Industries gain ground.

Vice President Vance Pushes for AI in Paris

This shift isn't happening in a vacuum, of course. The Trump administration, with Vice President JD Vance at the forefront, is actively pushing for AI development while taking a notably different approach from our European allies.

At the AI Action Summit in Paris last week, Vance made it clear that the U.S. won't let excessive regulation stifle innovation in this critical sector. “We need our European friends in particular to look to this new frontier with optimism rather than trepidation,” Vance told the audience, which included world leaders, CEOs and scientists from over 100 countries.

This pro-growth stance has already benefited U.S. chipmakers like Intel (NASDAQ:INTC), whose shares ended last week up more than 23% on news of increased support for domestic chip production. The company has its work cut out for it: Today, some 90% of the world’s most advanced chips are made by the Taiwan Semiconductor Manufacturing Company (TSMC).

Even Google, once hesitant about military contracts, has reversed its stance on AI weapons development. This shift signals a broader change in Silicon Valley's relationship with defense contracts, opening up new investment opportunities in tech companies that previously stayed away from the sector.

Europe’s Defense Tech Boom Is Just Getting Started

The transformation isn't limited to the U.S. Facing its own security challenges with Russia, Europe is seeing unprecedented growth in defense tech investment. Venture capital (VC) funding in defense technology hit a record $5.2 billion in 2024, according to a new report by Dealroom data. This marks an incredible fivefold jump from six years ago, making defense one of the fastest growing VC sectors in Europe right now.

For investors, this creates what I see as a once-in-a-generation opportunity. Defense Secretary Pete Hegseth's target of 3% of GDP for defense spending—roughly $1 trillion annually—suggests sustained government investment in the sector, despite Musk’s promise to cut costs. The key question isn't whether there will be spending, but rather which companies will capture it.

Positioning for the Biggest Defense Tech Shift in Decades

So where should investors be looking? I see three key areas:

First, companies at the intersection of AI and defense, like Palantir, that are already proving their worth in military applications. These firms are positioning themselves as essential partners in modern warfare capabilities.

Second, domestic semiconductor manufacturers like Intel that are critical to both AI development and national security. The Trump administration's focus on U.S. production could provide significant tailwinds for these companies.

And third, emerging defense tech companies that are disrupting traditional military procurement. While many are not publicly traded yet—Anduril being one such example—keeping an eye on this space could reveal early opportunities as they come to market.

We're witnessing the biggest transformation in defense technology since the advent of nuclear weapons, and I believe that those who position themselves in this new “AI arms race” could see substantial returns as this multi-decade trend unfolds.

***

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2024): General Dynamics Corp (NYSE:GD)., Taiwan Semiconductor Manufacturing Co. Ltd., Alphabet (NASDAQ:GOOGL) Inc.