Goldman Sachs (NYSE:GS) recently analyzed the implications of a report by ET Now on the potential exclusion of hybrid car tax concessions from the upcoming GST council meeting agenda. The Finance Ministry is not expected to discuss lowering the Goods and Services Tax (GST) for hybrid vehicles in its next meeting, despite a request in February 2024 from the Union Minister for Road Transport and Highways. The minister had urged a reduction in the GST rate for hybrid cars to 12%, down from the current 28% to 45%, depending on the vehicle’s size and engine capacity.

Currently, hybrid cars represent about 2% of monthly car sales in India, similar to electric vehicles (EVs), which benefit from a lower 5% GST rate. Major automakers like Maruti Suzuki (NS:MRTI), Toyota, and Honda produce hybrid vehicles, while Tata Motors (NS:TAMO), MG Motor, and Mahindra lead in the electric vehicle segment due to the favorable tax environment.

Offer: Click here to unlock powerful insights with InvestingPro! Assess stock health with over 100 parameters, get actionable ProTips, and discover the fair value of stocks—all for just INR 216/month with a 69% limited-time discount. Invest smarter and make informed decisions effortlessly!

Maruti Suzuki India:

Goldman Sachs maintains a neutral rating on Maruti Suzuki with a 12-month price target (PT) of INR 12,000, based on a price-to-earnings (P/E) valuation methodology. The valuation is pegged at 23 times the P/E ratio, consistent with historical medians applied to Q5 to Q8 earnings per share (EPS) estimates.

Upside Risks for Maruti Suzuki:

Positive reception of upcoming SUV launches.

Improved margins due to favorable raw material costs.

Revival in domestic demand for small cars.

Downside Risks for Maruti Suzuki:

Lagging behind Tata Motors and Mahindra in EV development.

Potential failure to make a significant impact with new SUV models.

Rising regulatory costs affecting small car affordability.

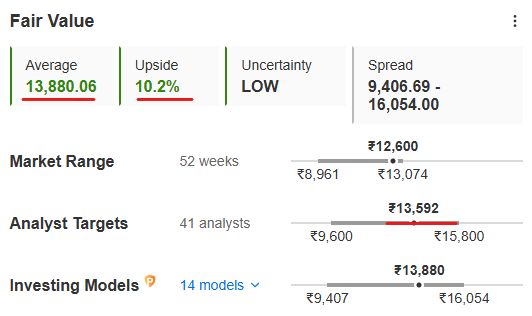

Image Source: InvestingPro+

While Goldman Sachs is not so bullish on Maruti Suzuki India, InvestingPro’s financial models are telling a different story. Keeping the news/rumors aside, and strictly from the valuation perspective, there is some good news for investors.

The fair value of the counter is INR 13,880, which depicts a healthy 10.2% upside from the CMP of INR 12,600.15. This value has been calculated after taking 14 different financial models into consideration, hence the reliability of it is much more than any single model.

Also, a total of 41 analysts are covering this counter and their combined average target is INR 13,592, pretty close to what the fair value is. Another thing to note is the financial health score of 4 out of 5 which denotes great performance on the fundamental front.

When all such information provided by InvestingPro is combined, investors can confidently make their investment decisions.

Click here and don’t miss out on the limited-time opportunity to subscribe to the industry-grade investment tool InvestingPro, now at a massive discount of 69%, for just INR 216/month.

Also Read: Breakout: Stock Breaks Trendline with a 5% Circuit

X (formerly, Twitter) - Aayush Khanna