From March 2022 through August 2024, there was widespread concern that the tightening of monetary policy by the Fed over that period would cause a recession. It was the most widely anticipated recession that didn’t happen on record. Once the Fed started easing monetary policy on September 18, 2024, it was widely expected that the Fed would have to lower interest rates significantly to avert a recession. Now that scenario has lost its credibility, especially following the lastest strong employment report for December.

The bond and stock markets have been recalibrating the outlook for the Federal Reserve’s monetary policy. The Fed cut the federal funds rate (FFR) by 100bps from September 18 through December 18 and signaled that more cuts are ahead in 2025. Bond market action suggests that investors have come around to our view that the Fed was stimulating an economy that didn’t need to be stimulated and that inflation was getting sticky north of the Fed’s 2.0% target. We argued that the economic and inflation data were signaling that the so-called neutral FFR was closer to 4.0%-5.0% than to 3.0%. We disagreed with the Fed’s view that the FFR was too restrictive when it was around 5.0%.

Our view has rapidly become the consensus view in recent weeks, especially after Friday’s strong employment report. That view can be described as a “higher-for-longer” interest-rate outlook, but “normal-for-longer” is the way we prefer to look at it. One of the reasons that we dissented over the past three years from the consensus forecast that a recession was coming is that we believed that the Fed’s monetary tightening simply brought interest rates back up to their normal levels in the years prior to the Great Financial Crisis and wouldn’t unduly stress the financial system, culminating in a recession.

In his September 18, 2024 press conference, Fed Chair Jerome Powell said that the 50bps cut in the FFR announced that day by the Federal Open Market Committee (FOMC) was simply a recalibration of monetary policy:

“So we know that it is time to recalibrate our policy to something that is more appropriate given the progress on inflation and on employment moving to a more sustainable level. So the balance of risks are now even. And this is the beginning of that process I mentioned, the direction of which is toward a sense of neutral, and we’ll move as fast or as slow as we think is appropriate in real time.”

We and our friends, the Bond Vigilantes, disagreed with the Fed’s recalibration. Our August 19 Morning Briefing was titled “Get Ready To Short Bonds?” We argued that the economy was in a soft patch that wouldn’t last too long. We predicted:

“Bond investors may be expecting too many interest-rate cuts too soon if in fact August’s economic indicators rebound from July levels and the Fed pushes back against the markets’ current expectations for monetary policy. So we are expecting to see the 10-year Treasury bond yield back in a range between 4.00% and 4.50% next month.”

Much to our consternation, instead of pushing back against the markets’ expectations, the Fed cut the FFR by 50bps on September 18 and Powell signaled that more rate cuts were coming. We pushed back against the Fed. Our October 15 Morning Briefing was titled “Will Fed Get Stuck With Sticky Inflation?” We wrote:

“By cutting interest rates despite strong economic growth, the Fed now risks overstimulating demand and reviving inflation. Services and wage inflation remain sticky, raising the risk that headline inflation gets stuck above 2.0%. The bond market agrees with our assessment that the Fed turned abruptly too dovish recently, boosting market expectations for long-term inflation higher.”

So now that the Fed has cut the FFR by 100bps since September 18, 2024, the 10-year bond yield is up 114bps since September 16, 2024. Even the 2-year Treasury note yield is up 91bps since September 24, 2024. Since the last FFR cut, on December 18, the number of additional 25bps rate cuts expected by the FFR futures market has declined from two to one over the next 12 months and none over the next six months.

")

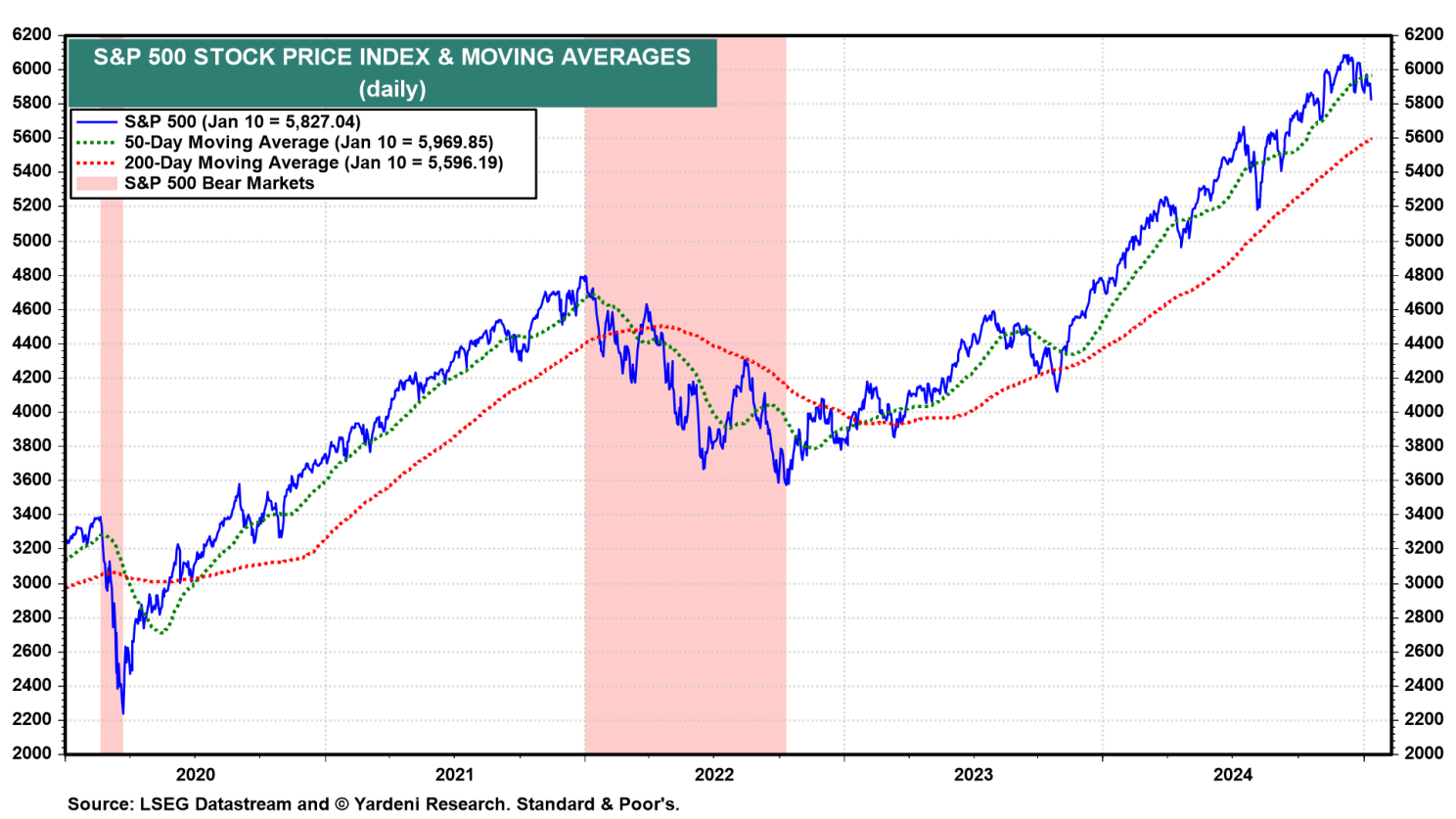

In early December, the stock market started to recalibrate the outlook for interest rates to higher-for-longer. The S&P 500 market-cap-weighted stock price index peaked at a record 6090.27 on December 6 and fell 4.3% through Friday’s close to 5827.04. It is 2.4% below its 50-day moving average.

(5) We anticipated this stock market correction at the end of last year. In the December 17 Morning Briefing, we wrote:

“With bullishness abounding, contrarian indicators are flashing red, and we see the potential for a market correction early next year.”

Our major concern was that the stock market was discounting too many FFR rate cuts, while the bond market was signaling that the Fed had already cut the rate by too much. Friday’s stock market rout suggests that stock investors have recalibrated their interest-rate outlook to higher-for-longer, a.k.a. normal-for-longer.

However, the downside may be short-lived. We are still expecting that the Q4-2024 earnings reporting season, which kicks into high gear this week, will show at least a 10% y/y increase in S&P 500 companies’ aggregate operating earnings per share. The analysts’ consensus is 8.2% currently.