TSX futures broadly steady ahead of Bank of Canada, Fed rate decisions

Goldman Sachs (NYSE:GS) recently analyzed Tata Power (NS:TTPW)'s performance in the fourth quarter of fiscal year 2024, noting that its adjusted profit after tax (PAT) of INR 4.7 billion fell slightly short of their estimate of INR 5 billion. This discrepancy was largely attributed to the decline in profitability in the coal business, which mirrored the global reduction in coal prices. Despite efforts to offset this through the Mundra (CGPL) segment, challenges persisted, particularly due to the imposition of Section 11, which disrupted the hedge.

The company's renewable capacity addition remained subdued during the quarter, with only 254MW added, bringing the total for the fiscal year to 597MW. However, management provided guidance for the execution of a 4.5GW pipeline by the end of fiscal year 2026 or early fiscal year 2027. Additionally, Tata Power stands to benefit from the domestic module usage mandate (ALMM) and the government's rooftop scheme, which could bolster its cell and module manufacturing business. Despite these potential opportunities, Goldman Sachs maintains a Sell rating for Tata Power, citing an unfavorable risk-reward profile at approximately 35x FY26E P/E.

Offer: Unlock the true value of stocks with InvestingPro by clicking here – your ultimate stock analysis tool! Say goodbye to inaccurate valuations and make informed investment decisions with accurate intrinsic value calculations. Get it now at a limited-time discount of 69%, only INR 216/month!

The fourth quarter saw Tata Power's consolidated adjusted PAT fall short of Bloomberg consensus estimates by 47% year-on-year. Declining profits in the coal mining segment, down approximately 26%, were primarily responsible for this miss, driven by the normalization of global coal prices. CGPL reported losses despite efforts to mitigate through Section 11, as the reduction in global coal prices limited the benefits of blending. However, the company received a one-time dividend of INR 3.3 billion from its subsidiary in Zambia and utilized INR 2.2 billion in tax credits during the quarter.

On the positive side, Tata Power's solar EPC business outperformed expectations, reporting a 45% increase in revenue year-on-year and an 84 basis points expansion in EBITDA margin. Management expressed optimism about the domestic rooftop solar scheme and the re-imposition of ALMM, which could drive further growth in the segment.

Despite these positives, Goldman Sachs revised its earnings estimates, anticipating a 10% earnings compound annual growth rate (CAGR) for FY23-26E. However, given the current valuation metrics, they maintain a Sell rating for Tata Power with an unchanged target price of INR 240 per share. Key upside risks include an increase in global coal prices and a favorable resolution of Mundra's challenges.

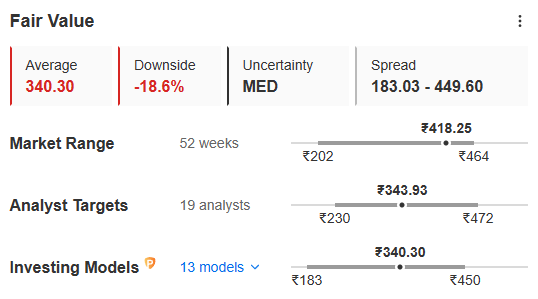

Image Source: InvestingPro+

The target price by Goldman Sachs might look a bit too much as it has a downside potential of 42%, from the CMP of INR 418. However, what’s more realistic way to calculate the fair value of a stock is to calculate the intrinsic value by various financial models and then taking a mean of all to negate extreme valuations.

This is exactly what the “fair value” feature of InvestingPro does, giving a more appropriate target price as per fundamental analysis. In the case of Tata Power, after carefully analyzing 13 financial models, the fair value comes at INR 340 per share, overvaluing the stock by 18.6%.

However, one thing to note is both Goldman Sachs and InvestingPro models are bearish on this counter which should make investors cautious.

Hurry up to grab your offer of 69% off on InvestingPro today by clicking here, before the limited-time discount is over!

Also Read: Pick: Stock Jumps 5%, Shows Strength for Higher Levels

X (formerly, Twitter) - Aayush Khanna