In its latest quarterly report, Bata India (NS:BATA) delivered a mixed performance that was slightly better than Goldman Sachs’ expectations but lagged behind its industry peers. The company's revenue grew by 2.5% year-on-year (YoY) in Q4, surpassing Goldman Sachs (NYSE:GS)' estimate of flat growth but falling short of Metro (TSX:MRU) Brands (NS:METB)' impressive 11% YoY increase.

Since FY22, Bata’s new management has focused on evolving the product portfolio to boost revenue growth, yet substantial results have been elusive. Despite aiming for double-digit revenue growth, Bata only managed a 1% increase in FY24, with a compound annual growth rate (CAGR) of 3.5% from FY19 to FY24.

Offer: Click here and don't miss out on this exclusive offer to access premium features of InvestingPro, including the powerful screeners, fair value calculator, financial health check, etc. and embark on your journey towards financial success. And the best part? InvestingPro is currently available at a 69% discount, priced at just INR 216/month.

During the Q4 earnings call, Bata's management revealed plans to cut approximately 20% of its product lines in stores during the second half of FY25. This significant reduction, aimed at eliminating redundancies, indicates the need for further portfolio adjustments before achieving the targeted double-digit revenue growth.

Bata's franchisee and e-commerce channels have been growth drivers, while the Company Owned Company Operated (COCO) channel and distribution network have been underperforming. The COCO channel, which accounts for about 70% of Bata’s revenues, showed weak same-store sales growth (SSSG) of 2.5% YoY despite a 4% increase in the number of stores. This underperformance persisted despite several strategic efforts, including closing unprofitable stores, enhancing the product portfolio, increasing advertising and promotional spending, investing in enterprise resource planning (ERP) systems, and renovating stores.

On the distribution side, which mainly serves the mass market, consumer demand remains weak, particularly for products priced below Rs500. Even though prices have remained stable for the past 5-6 quarters, the mass discretionary segment continues to struggle due to inflation and price hikes that have squeezed middle-income consumers' wallets. However, Bata anticipates some recovery in this segment starting in the second half of FY25 as affordability improves.

Goldman Sachs has adjusted its earnings per share (EPS) estimates for Bata, lowering them by about 5-7% for FY25-26, reflecting a delayed recovery in the company’s growth trajectory. They now project YoY revenue growth of approximately 7% for FY25 and 8% for FY26, compared to the consensus estimates of 10-11%.

Bata is valued at a long-term average price-to-earnings (P/E) multiple of 45x, which is a 30% discount to Metro Brands' core business valuation. Consequently, Goldman Sachs maintains a 12-month target price of Rs1,470 for Bata and a 'Neutral' rating, citing limited upside potential relative to the sector.

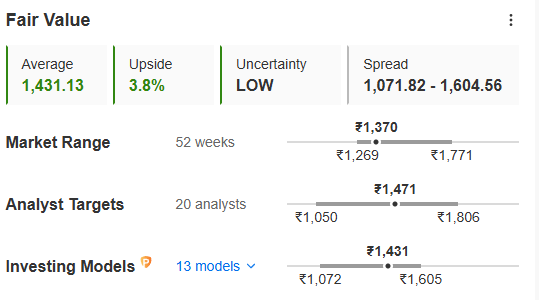

Image Source: InvestingPro+

While Goldman Sachs is slightly bullish on the counter, giving an upside potential of 7%, InvestingPro’s proprietary financial models are estimating an upside of 4% to INR 1,431 per share. This fair value has been calculated after considering 13 models and then taking an average of all of them to negate any outlier valuation.

Investors do not have to wait for the brokerages to come out with a report for fair valuation on any stock. They can simply look at the true intrinsic value if any counter in InvestingPro.

Even the average analyst’s target of 20 is also not quite high, at just INR 1,471. All these low valuation gaps can become a good indication to wait for some more correction in case investors are willing to bet on Bata India. This is a good framework investors can follow in their investing journey.

What’s more interesting? InvestingPro is now available at a massive 69% discount, for just INR 216/month. Click here and grab your limited-time offer today!