Rail freight transportation in India is poised for significant growth, with expectations of a notable increase in market share from 29% in F24 to 35% in F31e. This projection comes on the heels of various policy initiatives aimed at bolstering the rail sector's capacity and efficiency. Morgan Stanley (NYSE:MS)'s analysis indicates that these efforts could lead to a rise in rail's contribution to India's freight modal mix over the coming years.

The anticipated surge in rail freight share is underpinned by several factors, including the implementation of Dedicated Freight Corridors (DFCs) and the government's focus on expanding rail infrastructure. With the commissioning of the western DFC and ongoing efforts to improve network efficiency, Morgan Stanley expects Concor's Return on Equity (RoE) to rise significantly, reaching 16.1% by F27.

Concor, a key player in India's rail freight sector, is expected to benefit from these developments. The company has reported robust volume growth, outperforming market expectations, and has been focusing on enhancing customer-centric solutions under new leadership. Morgan Stanley highlights Concor's potential to reverse its market share loss trend through initiatives such as increasing cargo under First Mile Last Mile (FMLM) service. Consequently, it has increased the target price from INR 729 to INR 1,076 per share.

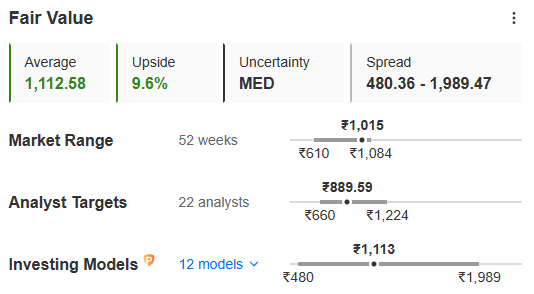

However, even before the target price increase, InvestingPro users could have gauged the realistic intrinsic value of the stock by looking at its fair value which is INR 1112 per share, depicting a 9.6% upside from the CMP of INR 1,015.

Fair value is a revolutionary feature that lets users know what actually the stock is worth via analyzing the counter through different complex financial models. You can do a lot more with InvestingPro, now available at a steep limited-time discount of up to 69%. Click here to make a move towards a better financial future.

Moreover, the imminent commissioning of the western DFC, particularly at JNPT port, is expected to drive further volume growth for Concor. This strategic move is anticipated to improve rail coefficient at JNPT from 18% to 30% over the next few years, significantly enhancing Concor's operational efficiency.

Despite these positive developments, Morgan Stanley notes that Concor's stock has seen a substantial increase in recent months, outperforming the broader market. Furthermore, the stock is currently trading at a relatively high PER of 32.5x F26e, suggesting limited upside potential in the near term.

Nevertheless, Concor remains a dominant player in an oligopolistic market, boasting a significant market share and a robust infrastructure network. The company's competitive advantages, including its extensive terminal network and cost-efficient operations, position it favorably for future growth.

Morgan Stanley's analysis underscores the promising outlook for India's rail freight sector, driven by infrastructure enhancements and policy support. While Concor stands to benefit from these developments, investors should consider the stock's current valuation and market dynamics before making investment decisions.

Also Read: Unlocking Investment Potential via Fair Value

X (formerly, Twitter) - Aayush Khanna